22 min read • Travel & transportation

Autonomous Mobility Journal Edition I I – August 2020

Arthur D. Little’s semi-annual coverage of the latest developments in autonomous mobility worldwide

Industry dynamics

Today, we live in a time when our daily lives are constantly shifting at a never-seen-before pace. This is largely driven by the huge technological leaps that are repetitively being achieved in different industries and parts of the globe. These advances are shaping the world of today and tomorrow, not only in the way we conduct our work and personal activities, but also in the way we tackle unforeseen events, such as the global COVID-19 pandemic of 2020.

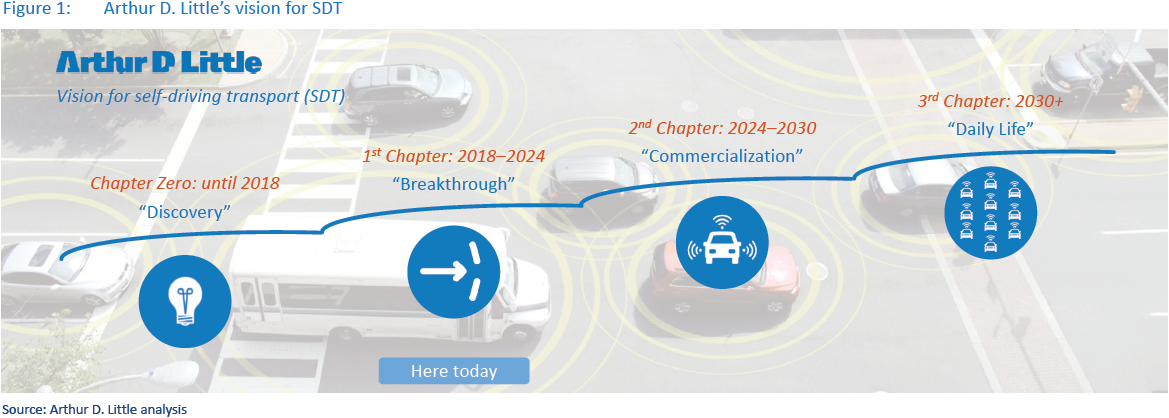

In transportation, myriad companies are racing to break the next barrier that will completely change the industry, and the world: autonomy. The initial Discovery phase, “Chapter Zero”, has already been crossed. We have now entered “Chapter 1”: Breakthrough. This chapter is the most crucial one, because it will define the finishing touches that will characterize transportation for decades to come. It will determine the losers, as well as the winners, that will reach the Commercialization phase (“Chapter 2”) with the best and most adequate technologies and operating models. As self-driving transport (SDT) matures, we will eventually reach the last and final chapter of the journey: Daily Life.

In this section of the journal, we will summarize our view of each of these chapters, followed by a brief update on the latest activities in SDT.

Chapter Zero: Discovery (until 2018)

Chapter Zero began earlier than most of us would think; research on self-driving vehicles dates back to as early as the 1900s, with the first promising experiments happening in the 1980s as part of the Navlab, Autonomous Land Vehicle (ALV) and Eureka Prometheus projects. However, it truly picked up once the required back-end technology had reached a sufficient level of maturity in the 2010s. Through Waymo, Google was one of the first to launch a self-driving vehicle program and achieve tangible results with hundreds of thousands of miles of autonomous driving. Big car manufacturers then joined the bandwagon, subsequently kick-starting the race for SDT.

As the awareness in SDT technologies and applications increased, original equipment manufacturers (OEMs), tech players and start-ups furthered their quests to improve SDT maturity and become the pioneers in their respective verticals. Venture capital (VC) funding in SDT start-ups further accelerated technology and capabilities acquisition. In parallel, governments and public sector entities kept pace with SDT innovations via nationwide programs and policies.

Chapter 1: Breakthrough (2018–2024)

With SDT’s maturity increasing day by day, we have now entered “Chapter 1”, with endless potential becoming more tangible now.

Although driver substitution is still limited and SDT’s usage is mostly restricted to geo-fenced areas, we are clearly entering a new phase of “Breakthrough”. No one can predict the end of this phase with certainty, since the application of technology presents many challenging aspects that still need to be solved from a legal, regulatory, operational and public acceptance perspective. A few examples of such challenges are:

- Legal/regulatory: Developing the required regulatory/ legal framework to address autonomous vehicle accident litigation. How much liability will the creators of the SDT algorithms/sensors bear?

- Operational: Setting the right infrastructure and systems to efficiently manage the network of cars that are both human driven and autonomous. Will human and non-human be able to coexist?

However, what is certain is that the necessary pieces are starting to come into place, laying the groundwork required for the commercialization of SDT, towards 2024. Indeed, gaps are slowly closing as transport-enabling industries refine their operating models (e.g., insurance, infrastructure) and different SDT players join forces through waves of alliances and M&As (e.g., Apple acquiring start-up Drive.ai in June 2019). Nevertheless, closing the gaps and practically realizing the true potential of artificial intelligence and SDT technology is still quite a complex task, which pushes investors to focus more towards larger players.

Chapter 2: Commercialization (2024–2030)

Around 2024, the SDT market is expected to reach the commercialization stage, with driverless vehicles seeing increased usage in the urban environment and reaching a significant share of vehicle sales across different verticals. As SDT increasingly interacts with the connected environment and seamlessly integrates into public transport, it will gain acceptance by society as the preferred and safest mode of transport. While this happens, clear market leaders, challengers and followers will start establishing deeper roots in the market. Who these players will be is anybody’s guess at this point.

Chapter 3: Daily Life (2030+)

Post-2030, the majority of transport vehicle sales will be SDcharacterized, beyond urban context and usage and spanning all areas and terrains. From this will emerge diversified technology giants, which will redefine the transport market. By the next decade, the urban-planning landscape and all related infrastructure and spacing will see itself transformed as SDT achieves full integration. This will lead to tangible impact on the economy via increased efficiency and shifts in cultural and societal trends.

Latest SDT transactions and trends

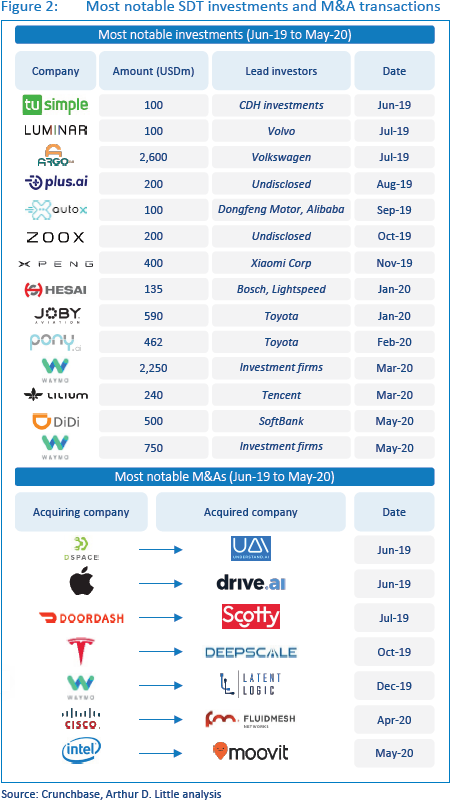

As mentioned in “Chapter 1”: Breakthrough, SDT players are continuing to combine their capabilities in different parts of the value chain through waves of alliances, M&As and investments. In our previous edition, we detailed several transactions that had occurred in 2018 and early 2019, such as Aptiv, a large transport technology company, acquiring KUM for USD 500 mn, and Rivian receiving a total of USD 1.6 bn in funding from huge players such as Cox Automotive, Ford and Amazon.

Since mid-2019, several interesting transactions have already happened, shedding light on the continuously evolving dynamics and trends in the SDT industry.

Technology giants and OEMs are continuing to invest in and acquire companies in order to gain access to technology and capabilities in their ongoing effort to get ahead in the race for SDT, which has proven to be more difficult than most thought. One of the most notable of such transactions was completed in July 2019 by Volkswagen Group, which invested USD 2.6 bn in Argo AI. Along with Ford’s investment in 2017, this brings Argo AI’s total money raised to USD 3.6 bn and represents the start of an alliance between the two car manufacturers, which have agreed to share the cost of achieving full autonomy. Along with Argo AI, two start-ups now clearly stand out and seem to have gotten well ahead in the race:

- Cruise has amassed a total of USD 5.3 bn since May 2019, with General Motors as its lead investor (USD 3.4 bn) and Honda Motor as its second (USD 750 mn).

- Through its recent investment rounds in March and May 2020, Google’s Waymo has now amassed a total of USD 3 bn, mainly through investment funds such as Silver Lake Partners and T. Rowe Price.

Similarly, to the Ford/Volkswagen/Argo AI alliance, other companies are also joining forces to deal with the high complexity and cash requirements of SDT. For example, Hyundai and Aptiv announced in 2019 that they would be establishing an evenly owned USD 4 bn joint venture (JV). Hyundai will contribute with cash and R&D, and Aptiv with its autonomous technology and experienced human capital.

Another interesting transaction was Apple’s acquisition of Drive. ai in June 2019, just days before its bankruptcy. Although very promising at first, the start-up was not able to survive the wave of consolidation and increased challenges, which allowed Apple to strategically access additional SDT technology and learnings at a low cost.

Although self-driving road cars remain the clear focus for companies around the world, we can now see other modes of SDT picking up interest. Indeed, both autonomous trucking and autonomous aerial taxi companies have seen an increase in investments in H2 2019 and H1 2020, respectively. In autonomous trucking, TuSimple and Plus.ai received USD 100 mn and USD 200 mn in investments, respectively. In autonomous aerial taxis, Lilium received a total of USD 240 mn in March 2020, with Tencent as its lead investor. However, Joby Aviation remains the clear leader after receiving a whopping USD 590 mn in a round led by Toyota, which invested a total of USD 394 mn in the company. Along with its investments in Pony.ai, Uber ATG and Didi Chuxing, and its new partnership with Chinese autonomous driving start-up Momenta, Toyota is diversifying in aerial taxis to expand its reach.

These trends come in parallel with the decrease in price of SDT sensors, especially LiDAR. For example, Luminar, which recently teamed up with Volvo, has announced its plans for reducing the cost of LiDAR to around USD 1,000 per unit, versus the current incredibly high cost of around USD 75,000. When achieved, such a decrease in cost will become a game changer for the SDT industry, which will be able to provide more competitive and affordable solutions.

Overall, the number of SDT and auto-tech deals seems to have remained steady in H2 2019 and the beginning of 2020. However, we are yet to see the true impact of COVID-19 on SDT.

On one hand, companies are struggling to absorb the economy’s alarming slowdown and inevitable recession to come. The global autonomous car market is expected to decrease at a CAGR of 3.19 percent from 2019 to 2020, mainly due to COVID-19 (although it is predicted to recover and grow at a CAGR of 16.84 percent until 2023). Additionally, Ford announced in April its decision to postpone its SD vehicle launch from 2021 to 2022 and is actively rethinking its go-to-market strategy.

On the other hand, the emergence of a global pandemic of this nature has greatly reinforced the need for autonomy and SDT. In times of diseases as transmissible and dangerous as COVID-19, the idea of having autonomous vehicles transporting people and goods becomes indispensable. Such technologies and applications could, indeed, greatly help in delivering medicine, food and people while maintaining strict social distancing requirements, and thus helping fight the spread of the virus. As the technology matures, governments will need to develop the necessary policies to integrate SDT within their pandemic emergency responses.

Use case of the semester

Focus on first- and last-mile (FLM) passenger transportation

Research in the US shows that the need to walk more than 800 m to the nearest transit stop reduces public transport trips by around 90 percent. Hence, transport authorities, OEMs, start-ups and technology companies are all investing in building first- and last-mile (FLM) transport solutions. Furthermore, driverless technology is expected to make these solutions even more efficient and safe. However, there are still a few challenges hindering wide-scale deployment of these solutions. In this context, Dubai launched its World Challenge for Self-Driving Transportation in 2018–19, with focus on FLM connection to test technology maturity and supporting technical development, public awareness and policy development.

First- and last-mile solutions

Transport authorities worldwide are encouraging FLM solutions, as they enable people to use public transportation. Companies are investing in developing and testing prototypes of autonomous FLM solutions to increase efficiency and safety on roads. Navya (France), EasyMile (France), 2getthere (the Netherlands), Westfield (the UK) and Gaussin (France) are the leading companies that offer the most advanced solutions in autonomous FLM transportation. Details of their offerings are captured in Figure 4.

As can be seen in the figure, the solutions still vary in technological maturity and technical specifications. All five offered solutions are SAE Level 4 in autonomous driving and currently being tested on designated routes in restricted zones, such as shuttle services for universities, airport connections and campuses of private companies. The growth of autonomous FLM transportation has also spurred activity among technology start-ups to develop vehicle-to-everything (V2X) connectivity, analytics, safety and smart solutions. Leading start-up players include Derq, Sensible 4 and iAuto.

Challenges in deployment of autonomous first- and last-mile transportation

Despite the technological advancement of autonomous shuttles, there are still a few challenges that hinder wide-scale deployment. The key challenges that transport authorities need to be mindful of to ensure successful adoption of driverless shuttles are:

- Building perception of safety and trust.

- Educating people on using the service and operating in public spaces.

- Building low-cost and environmentally sustainable charging options.

- Handling the fear of driver job losses.

- Ensuring financial sustainability of the business.

- Influencing pedestrians, cyclists and other vehicle users’ behavior.

To address these challenges, public transport authorities need to proactively develop policy frameworks and strategies to shape the autonomous FLM transportation segment. Since autonomous FLM transportation technology is in nascent stages of development and adoption, authorities need to invest in building adequate ecosystems via levers such as adaptive regulations, funding, capabilities building, organizing competitions to encourage innovation, testing autonomous technologies/infrastructure, and creating public awareness.

Dubai World Challenge for Self-Driving Transportation

(Focus on FLM connections)

Dubai has been at the forefront of the autonomous transportation wave and aspires to have 25 percent of all its transportation trips as smart and driverless by 2030. To realize this vision, Dubai’s Roads and Transport Authority (RTA) launched the “Dubai Autonomous Transportation Strategy”. As part of the strategy, Dubai organized its World Challenge for Self-Driving Transportation in 2018–19 as a global RFP to encourage the world’s most innovative international companies, academic institutions and centers of R&D to test the latest advances in this technology by providing transportation solutions and scenarios that were realistic and tailored for Dubai. The challenge was launched with a focus on first-/last-mile transportation:

- Objectives: The challenge aimed at providing a platform to leading players to showcase their automated driving technologies for first-/last-mile connections, demonstrate use cases, and support technical development, public awareness and policy development. In addition, it helped showcase Dubai’s brand as an international leader in transport and smart city technology.

- Use cases: Three use cases were identified: (a) self-driving vehicles (SDVs) connecting origin/destination to public transport, (b) SDVs connecting off-site parking lots to venue entrances, and (c) SDVs transporting people around certain locations/developments.

- Participants: Out of 65 initial participants, five leaders (SDV manufacturers Gaussin, Westfield, Navya, 2getthere and EasyMile), three start-ups (Derq, Sensible 4 and iAuto) and eight academic bodies (local universities – Abu Dhabi University, Al Ain University, UAEU, University of Dubai; and international universities – Carnegie Melon University, University of Technology Sydney, Universidad Carlos III de Madrid, University of Berlin) were selected for the challenge.

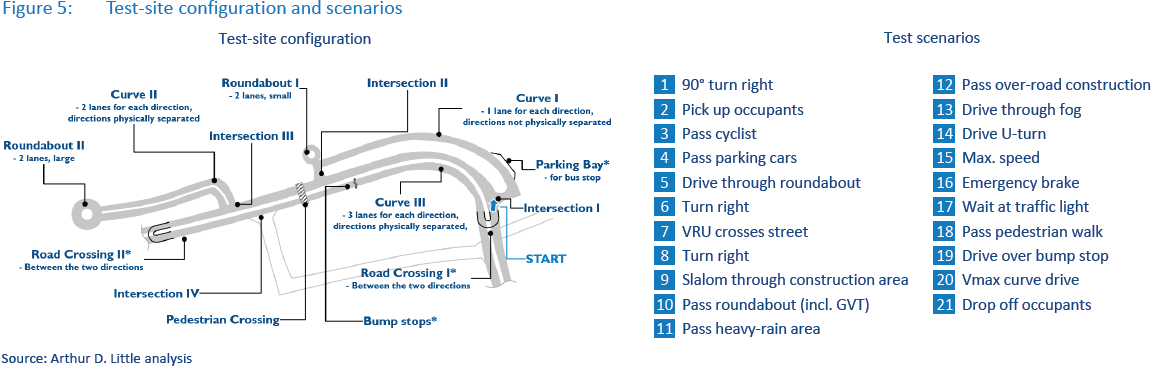

- Testing: A testing site was chosen based on access, testsite architecture, infrastructure and flexibility/availability. Twenty-one test cases were set up at the circular test track to be performed by the vehicle under test. (Please refer to Figure 5 for more details on the track and test cases). Participants drove the circular tour multiple times, with its complexity increasing with every round. Examples of complexity levers were speed levels, Dubai-specific environment constraints, staged mixed traffic, and obstacles (e.g., parking cars, construction zones). The vehicle under test was equipped with measuring equipment to record key evaluation parameters such as position, speed, acceleration, and time.

- Evaluation: Each participant group had to deliver a presentation to demonstrate its technical capabilities. However, since each participant group had different levels of technological maturity, different testing focus and procedures were applied:

- Leaders tested their vehicles on the challenge test track.

- Start-ups gave live demonstrations of technology functionality.

- Academia focused on demonstrating work-model functionality – either live or in simulation.

Participants were evaluated on seven competence fields – business model, endurance and reliability, energy efficiency and environmental suitability, consumer experience, safety & cyber security, staged mix-traffic, and simulation and new concepts. As an output of the evaluation, Navya and Gaussin were the winners in the Leaders category, with Navya’s vehicle demonstrating high durability and reliability and displaying exemplary customer experience, and Gaussin’s vehicle ranking highest in energy and sustainability.

A key learning from the Dubai SDT challenge was that one of the biggest hurdles in autonomous FLM transportation was passenger safety. The Roads and Transport Authority in Dubai recognized this concern and made it a topmost priority. They tested the autonomous technologies in different use-case scenarios and constraints, simulating different possibilities for obstacles faced on roads. The challenge received global acknowledgement for its robust testing approach and was a big success, attracting more than 700 technology leaders and innovators, as well as around 3,000 visitors for the accompanying exhibition.

City of the semester

Focus on Dubai

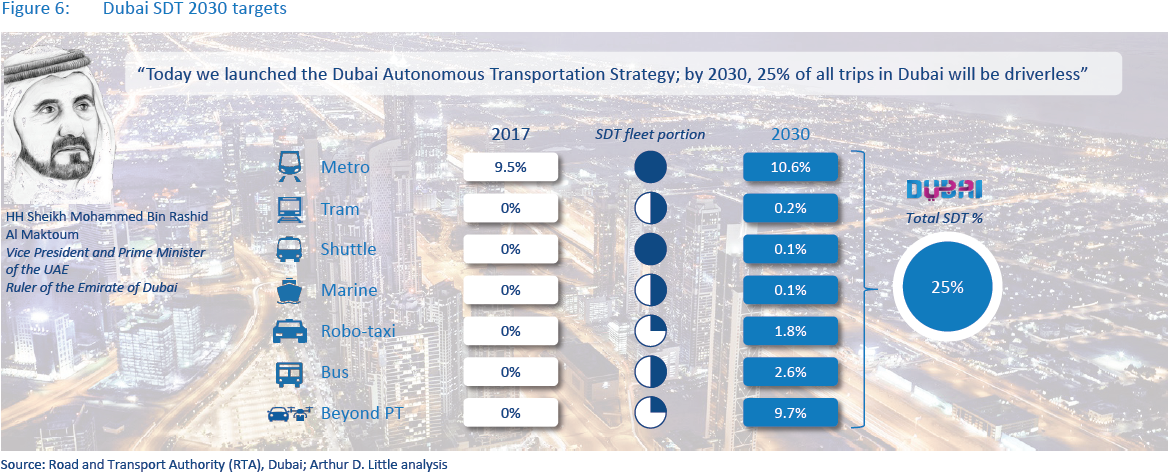

Autonomous technology is redefining the future of urban mobility and public transport. A revolution is on the horizon, from cars to buses to marine transport. OEMs, technology companies and transport authorities are joining the race to deploy selfdriving transport, establish their leadership positions in this fast-paced environment, and reap the multiple benefits it can deliver. In this context, the Road and Transportation Authority (RTA) of Dubai has defined the Dubai Self-Driving Transport (SDT) Strategy, which aims to achieve 25 percent of all transportation trips in Dubai as smart and driverless by 2030.

Dubai Self-Driving Transport Strategy overview

As a part of Dubai’s smart city strategy, His Highness Sheikh Mohammad bin Rashid Al Maktoum launched the Dubai Smart Self-Driving Vision, stating, “By 2030, 25 percent of all trips in Dubai will be driverless.”

To achieve this ambitious vision, RTA has developed the Dubai Self-Driving Transport (SDT) Strategy, which provides a vision, roadmap, and policy framework comprising a strategy for testing, development, and deployment of SDT.

The uniqueness of the Dubai SDT Strategy is its focus on multimodal transportation. Indeed, while most other cities and countries are focusing on selected transportation modes, Dubai is targeting SDT across all modes of public transport, including metro, tram, bus, taxi, marine transport, cable cars and shuttle.

As depicted in Figure 6, the self-driving Metro is currently the only transport mode contributing towards SDT, accounting for approximately 9.5 percent of all individual trips in Dubai. However, by 2030, the 25 percent target will be achieved via application of SDT technologies to other transport modes.

Dubai Self-Driving Strategy roadmap

RTA has developed a comprehensive Dubai SDT roadmap that considers not only SDT technology readiness, but also the infrastructure and legal requirements at the base of SDT deployment.

In addition, the Dubai SDT roadmap has been tested with the support of SDT experts in the field of SDT technology, as well as infrastructure and insights drawn from conducting a series of workshops with the major OEMs and start-ups leading the SDT ecosystem.

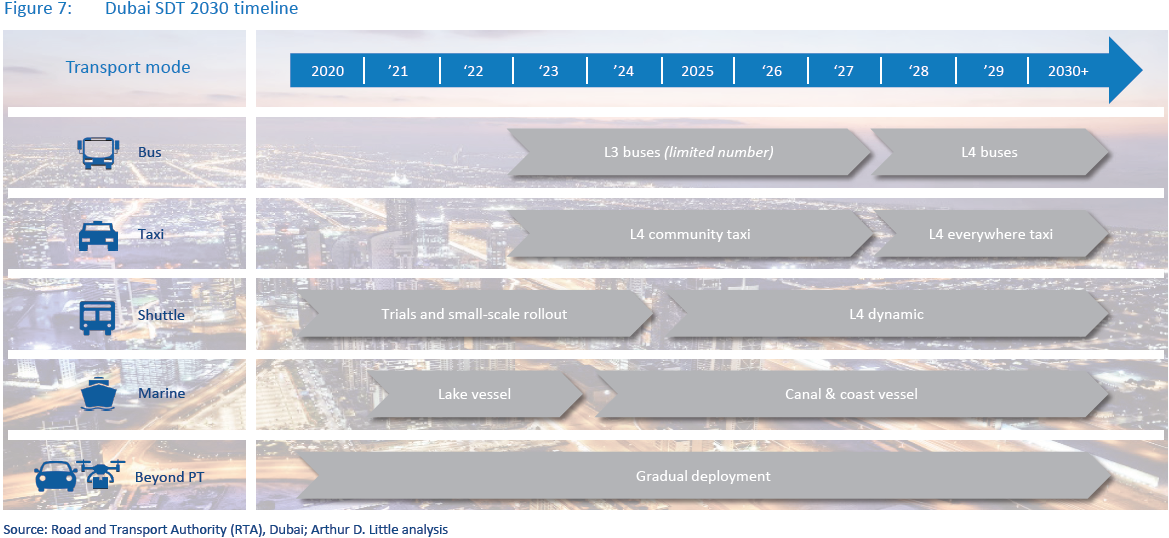

For each transportation mode, the following implementation plan will be executed in Dubai, to achieve 25 percent SDT by 2030:

- Bus transport mode

- In 2023, RTA will start conducting the first commercial trials of a limited number of L3 smart buses. L3 smart buses will require the presence of a human driver. Operation in automated mode will be possible only in simple operational design domains (ODDs), with limited interaction with mixed traffic.

- In 2028, RTA will launch the first L4 buses. L4 buses will be driverless and capable of operating in automated mode in simple and complex ODDs (e.g., complex urban roads), with full interaction with mixed traffic.

- Taxi transport mode

- In 2023, RTA will introduce L4 community taxis. L4 community taxis will be driverless and capable of operating in automated mode only in limited ODDs, within some communities of the city of Dubai (e.g., Jumeirah Lake Towers, Downtown).

- In 2028, RTA will launch L4 “everywhere” taxis. L4 everywhere taxis will be driverless and capable of operating in automated mode across all HD-mapped areas of Dubai in both simple and complex ODDs.

- Shuttle transport mode

- In 2020, RTA will conduct the first trials and start small rollouts of L4 shuttles. L4 shuttles will be driverless and capable of operating in automated mode only in very simple ODDs, with limited interaction with mixed traffic.

- In 2025, RTA will introduce L4 dynamic shuttles. At this stage, shuttles will still be driverless and able to operate in automated mode on both simple and complex urban roads, with full interaction with mixed traffic. In addition, these vehicles will operate on pre-programmed routes with dynamic features

- Marine transport mode

- In 2021, RTA will introduce lake vessels, autonomous electric abras that will operate on the artificial lakes of Dubai (e.g., Burji Khalifa, Global Village). These vessels will not require the presence of supervisors on board but be remotely supervised by operators from an operation control center (OCC).

- In 2024, Dubai will introduce canal and coast vessels, autonomous vessels which will operate along the coast and canals of the Dubai. These vessels will require human presence on board, but only in an engineering/ safety role. These vessels will still be remotely supervised by operators from an OCC.

- Beyond public transport

- Beyond public transport, other modes, such as personal SDT passenger vehicles, autonomous aerial taxis, SDT logistic bots, and SDT logistic drones, will be gradually introduced to contribute towards the achievement of the 25 percent by 2030.

The implementation plan does not include Metro and other rail public transportation modes since their systems are already automated.

Dubai Self-Driving Strategy enablers

To accomplish its vision, Dubai should focus on the following self-driving strategy enablers to guarantee execution of its ambitious implementation plan:

- Regulatory readiness: Dubai should lead in developing policies and legislation to allow full operation of selfdriving vehicles on its public streets. Legal and regulatory components such as liability and insurance, data privacy and cybersecurity, and SDT vehicle licensing and registration should be amended in order to accelerate SDT rollout.

- Infrastructure readiness: Better and smart public transport infrastructure elements such as service depots, vehicle stops, and road layouts will be required to allow implementation and operation of SDT vehicles. These are some elements that RTA needs to be mindful of when planning future SDT rollout.

- Technology/system readiness: SDT deployment also requires enhancement of certain technology/system elements such as control centers, fare collection systems, network connectivity, cyber security and HD maps. These will enable vehicle connectivity and ensure a safe SDT rollout.

- Customer acceptance: Creating customer acceptance is key for SDT deployment. The biggest hurdles to customers’ acceptance are their concerns about the cybersecurity of connected cars and the reliability of cars with autonomous functions. Dubai should conduct several surveys and focus groups to understand how to increase the overall acceptance of SDT.

Interview of the semester

Interview with Joby Aviation’s Executive Chairman by Antonio Semeraro – Manager at Arthur D. Little Middle-East

Joby Aviation is a venture-backed aerospace company that is developing and commercializing a piloted all-electric vertical take-off and landing (eVTOL) aircraft that can enable a fast, quiet, and affordable air-taxi service. Joby Aviation competes against other companies developing eVOTL aircrafts, mainly large traditional companies such as Bell, Boeing and Airbus, and start-ups such as Lilium and Volocopter. It distinguishes itself with its relatively mature aircraft technology and service offering. The company claims it is “100 times quieter than conventional aircraft during take-off and landing, and near-silent when flying overhead.” Last January, it raised another USD 590 mn in a Series C funding round led by Toyota Ventures, which increased its total funding to USD 721 mn. We had the pleasure of conducting an e-interview with Paul Sciarra, the executive chairman at Joby Aviation and co-founder of Pinterest.

Mr. Paul Sciarra is the executive chairman of Joby Aviation and co-founder of Pinterest

Mr. Paul Sciarra is the executive chairman of Joby Aviation and co-founder of Pinterest

Q: Could you give us a brief background on Joby?

A: Joby Aviation is an aerospace company that is developing and commercializing a piloted all-electric vertical takeoff and landing (eVTOL) aircraft that can enable fast, quiet, and affordable air-taxi service. Ten years ago, we set out to improve daily transportation. Increased congestion, underfunded infrastructure, and rising emissions led us to design a new class of electric aircraft – one that can get you to where you are going up to five times faster than driving, at a cost that can approach car travel, and with zero emissions.>/p>

Q: How do you define Urban Air Mobility (UAM) at Joby? What is your vision?

A: “Urban air mobility” was coined by NASA and most recently changed to “advanced air mobility” – you can read more about it here: https://www.nasa.gov/aam.

Our vision is to bring fast, quiet and zero-emissions air mobility to communities worldwide that will change how we connect people with the places they live, work, and play in.

We’re happy that the industry has shifted from just urban air mobility to advanced air mobility. Everyone – whether in cities, suburbs or rural communities – wants to get where they are going more quickly. If the problem in cities is overcrowded roads, the problem in some rural areas is non-existent ones or inconvenient routing. We’ve designed a vehicle that we believe can solve both problems for both types of communities.

Q: What is the target position of Joby in the UAM ecosystem?

A: First, the aircraft.

We are bringing to market the most advanced and comfortable eVTOL aircraft, optimized for air-taxi operations.

Then, the service.

We will not only build the vehicles, but also operate them in communities worldwide.

Q: Why do you see great potential for UAM, and what future use cases do you see?

A: We aim to deliver safe, quiet and increasingly affordable air transportation to everyone, for any trips two to 150 miles. Those could be one-off trips or your daily commute. We want to make it faster and safer to get you where you’re going.

Q: How do you envision the future business model of UAM?

A: We’re not only designing, building and certifying the aircraft; we’re also operating the service – delivering air transportation directly to passengers.

In many ways, it’s actually a not-uncommon model in the history of aviation. In the early days of air travel, Boeing owned United. They not only designed and built airplanes, but also operated them as a commercial carrier. We’re heading “back to the future” with this approach.

Q: For UAM deployment in a city, who are the main stakeholders involved in the deployment and what are their roles? How can different stakeholders work together to support aerial vehicle deployment?

A: We’re actively working with several city governments, local communities and private property owners to build support and infrastructure for the service. It’s still early, but the reception, so far, has been encouraging.

Q: Which vehicle will Joby introduce initially?

A: Joby Aviation’s aircraft is designed for four passengers plus a pilot. We made the decision very early to make provisions for a trained pilot in-seat – both to ensure our passengers feel safe and comfortable, and to ease integration with existing air-traffic control (which is still based on humans talking to other humans over radio).

Q: Where do you see UAM being implemented initially? Has Joby identified potential markets for initial operations?

A: We expect to see AAM initially implemented on routes that have a lot of people moving in both directions. Airports to city centers are a good example. Nearby city-pairs are another.

We are not quite ready to discuss details of Joby’s initial launch markets. We can say we’re actively evaluating several options.

Q: What is the main issue regarding public acceptance, and what steps can be taken to overcome this?

A: It’s critically important that we earn the public’s trust when it comes to the safety of our vehicle. We started with the design, which is doubly and, in some cases, triply redundant across all critical subsystems to avoid any single points of failure. We’ve begun the type certification process with the US FAA to ensure – through rigorous testing at the component, the subsystem and the vehicle level – that the aircraft meets or exceeds the highest safety and reliability standards.

Q: What is the major challenge going forward?

A: Right now, we are squarely focused on certifying the aircraft and getting ready for initial production of the aircraft. We expect to break ground on a new factory shortly.

We’re in the hard business of aircraft development and certification because the right certified vehicle is the key to unlocking this market.

Q: How are different regulators responding to UAM deployment?

A: Joby has been working with the FAA for several years and began a formal type certification program in 2018. The type certification process assures the safety of the vehicle and typically takes three to five years.

We’ve been extremely impressed with the diligence and creativity of our counterparts at the FAA. Fundamentally, they care about the same thing we care about: the safety of the aircraft and its passengers.

Joby is also in discussion with a number of international regulators regarding the parallel certification paths and ex-US, commercial operation of our aircraft.

Q: What is/will likely be the key impact of COVID-19 on your business and the autonomous industry in general?

A: It’s hard to predict the impact of COVID-19 on our business as we look ahead to commercial launch, a few years away.

Right now, we’re focused on ensuring our employees are safe, and contributing where we can in the communities where we operate.

DOWNLOAD THE FULL REPORT

22 min read • Travel & transportation

Autonomous Mobility Journal Edition I I – August 2020

Arthur D. Little’s semi-annual coverage of the latest developments in autonomous mobility worldwide

DATE

Industry dynamics

Today, we live in a time when our daily lives are constantly shifting at a never-seen-before pace. This is largely driven by the huge technological leaps that are repetitively being achieved in different industries and parts of the globe. These advances are shaping the world of today and tomorrow, not only in the way we conduct our work and personal activities, but also in the way we tackle unforeseen events, such as the global COVID-19 pandemic of 2020.

In transportation, myriad companies are racing to break the next barrier that will completely change the industry, and the world: autonomy. The initial Discovery phase, “Chapter Zero”, has already been crossed. We have now entered “Chapter 1”: Breakthrough. This chapter is the most crucial one, because it will define the finishing touches that will characterize transportation for decades to come. It will determine the losers, as well as the winners, that will reach the Commercialization phase (“Chapter 2”) with the best and most adequate technologies and operating models. As self-driving transport (SDT) matures, we will eventually reach the last and final chapter of the journey: Daily Life.

In this section of the journal, we will summarize our view of each of these chapters, followed by a brief update on the latest activities in SDT.

Chapter Zero: Discovery (until 2018)

Chapter Zero began earlier than most of us would think; research on self-driving vehicles dates back to as early as the 1900s, with the first promising experiments happening in the 1980s as part of the Navlab, Autonomous Land Vehicle (ALV) and Eureka Prometheus projects. However, it truly picked up once the required back-end technology had reached a sufficient level of maturity in the 2010s. Through Waymo, Google was one of the first to launch a self-driving vehicle program and achieve tangible results with hundreds of thousands of miles of autonomous driving. Big car manufacturers then joined the bandwagon, subsequently kick-starting the race for SDT.

As the awareness in SDT technologies and applications increased, original equipment manufacturers (OEMs), tech players and start-ups furthered their quests to improve SDT maturity and become the pioneers in their respective verticals. Venture capital (VC) funding in SDT start-ups further accelerated technology and capabilities acquisition. In parallel, governments and public sector entities kept pace with SDT innovations via nationwide programs and policies.

Chapter 1: Breakthrough (2018–2024)

With SDT’s maturity increasing day by day, we have now entered “Chapter 1”, with endless potential becoming more tangible now.

Although driver substitution is still limited and SDT’s usage is mostly restricted to geo-fenced areas, we are clearly entering a new phase of “Breakthrough”. No one can predict the end of this phase with certainty, since the application of technology presents many challenging aspects that still need to be solved from a legal, regulatory, operational and public acceptance perspective. A few examples of such challenges are:

- Legal/regulatory: Developing the required regulatory/ legal framework to address autonomous vehicle accident litigation. How much liability will the creators of the SDT algorithms/sensors bear?

- Operational: Setting the right infrastructure and systems to efficiently manage the network of cars that are both human driven and autonomous. Will human and non-human be able to coexist?

However, what is certain is that the necessary pieces are starting to come into place, laying the groundwork required for the commercialization of SDT, towards 2024. Indeed, gaps are slowly closing as transport-enabling industries refine their operating models (e.g., insurance, infrastructure) and different SDT players join forces through waves of alliances and M&As (e.g., Apple acquiring start-up Drive.ai in June 2019). Nevertheless, closing the gaps and practically realizing the true potential of artificial intelligence and SDT technology is still quite a complex task, which pushes investors to focus more towards larger players.

Chapter 2: Commercialization (2024–2030)

Around 2024, the SDT market is expected to reach the commercialization stage, with driverless vehicles seeing increased usage in the urban environment and reaching a significant share of vehicle sales across different verticals. As SDT increasingly interacts with the connected environment and seamlessly integrates into public transport, it will gain acceptance by society as the preferred and safest mode of transport. While this happens, clear market leaders, challengers and followers will start establishing deeper roots in the market. Who these players will be is anybody’s guess at this point.

Chapter 3: Daily Life (2030+)

Post-2030, the majority of transport vehicle sales will be SDcharacterized, beyond urban context and usage and spanning all areas and terrains. From this will emerge diversified technology giants, which will redefine the transport market. By the next decade, the urban-planning landscape and all related infrastructure and spacing will see itself transformed as SDT achieves full integration. This will lead to tangible impact on the economy via increased efficiency and shifts in cultural and societal trends.

Latest SDT transactions and trends

As mentioned in “Chapter 1”: Breakthrough, SDT players are continuing to combine their capabilities in different parts of the value chain through waves of alliances, M&As and investments. In our previous edition, we detailed several transactions that had occurred in 2018 and early 2019, such as Aptiv, a large transport technology company, acquiring KUM for USD 500 mn, and Rivian receiving a total of USD 1.6 bn in funding from huge players such as Cox Automotive, Ford and Amazon.

Since mid-2019, several interesting transactions have already happened, shedding light on the continuously evolving dynamics and trends in the SDT industry.

Technology giants and OEMs are continuing to invest in and acquire companies in order to gain access to technology and capabilities in their ongoing effort to get ahead in the race for SDT, which has proven to be more difficult than most thought. One of the most notable of such transactions was completed in July 2019 by Volkswagen Group, which invested USD 2.6 bn in Argo AI. Along with Ford’s investment in 2017, this brings Argo AI’s total money raised to USD 3.6 bn and represents the start of an alliance between the two car manufacturers, which have agreed to share the cost of achieving full autonomy. Along with Argo AI, two start-ups now clearly stand out and seem to have gotten well ahead in the race:

- Cruise has amassed a total of USD 5.3 bn since May 2019, with General Motors as its lead investor (USD 3.4 bn) and Honda Motor as its second (USD 750 mn).

- Through its recent investment rounds in March and May 2020, Google’s Waymo has now amassed a total of USD 3 bn, mainly through investment funds such as Silver Lake Partners and T. Rowe Price.

Similarly, to the Ford/Volkswagen/Argo AI alliance, other companies are also joining forces to deal with the high complexity and cash requirements of SDT. For example, Hyundai and Aptiv announced in 2019 that they would be establishing an evenly owned USD 4 bn joint venture (JV). Hyundai will contribute with cash and R&D, and Aptiv with its autonomous technology and experienced human capital.

Another interesting transaction was Apple’s acquisition of Drive. ai in June 2019, just days before its bankruptcy. Although very promising at first, the start-up was not able to survive the wave of consolidation and increased challenges, which allowed Apple to strategically access additional SDT technology and learnings at a low cost.

Although self-driving road cars remain the clear focus for companies around the world, we can now see other modes of SDT picking up interest. Indeed, both autonomous trucking and autonomous aerial taxi companies have seen an increase in investments in H2 2019 and H1 2020, respectively. In autonomous trucking, TuSimple and Plus.ai received USD 100 mn and USD 200 mn in investments, respectively. In autonomous aerial taxis, Lilium received a total of USD 240 mn in March 2020, with Tencent as its lead investor. However, Joby Aviation remains the clear leader after receiving a whopping USD 590 mn in a round led by Toyota, which invested a total of USD 394 mn in the company. Along with its investments in Pony.ai, Uber ATG and Didi Chuxing, and its new partnership with Chinese autonomous driving start-up Momenta, Toyota is diversifying in aerial taxis to expand its reach.

These trends come in parallel with the decrease in price of SDT sensors, especially LiDAR. For example, Luminar, which recently teamed up with Volvo, has announced its plans for reducing the cost of LiDAR to around USD 1,000 per unit, versus the current incredibly high cost of around USD 75,000. When achieved, such a decrease in cost will become a game changer for the SDT industry, which will be able to provide more competitive and affordable solutions.

Overall, the number of SDT and auto-tech deals seems to have remained steady in H2 2019 and the beginning of 2020. However, we are yet to see the true impact of COVID-19 on SDT.

On one hand, companies are struggling to absorb the economy’s alarming slowdown and inevitable recession to come. The global autonomous car market is expected to decrease at a CAGR of 3.19 percent from 2019 to 2020, mainly due to COVID-19 (although it is predicted to recover and grow at a CAGR of 16.84 percent until 2023). Additionally, Ford announced in April its decision to postpone its SD vehicle launch from 2021 to 2022 and is actively rethinking its go-to-market strategy.

On the other hand, the emergence of a global pandemic of this nature has greatly reinforced the need for autonomy and SDT. In times of diseases as transmissible and dangerous as COVID-19, the idea of having autonomous vehicles transporting people and goods becomes indispensable. Such technologies and applications could, indeed, greatly help in delivering medicine, food and people while maintaining strict social distancing requirements, and thus helping fight the spread of the virus. As the technology matures, governments will need to develop the necessary policies to integrate SDT within their pandemic emergency responses.

Use case of the semester

Focus on first- and last-mile (FLM) passenger transportation

Research in the US shows that the need to walk more than 800 m to the nearest transit stop reduces public transport trips by around 90 percent. Hence, transport authorities, OEMs, start-ups and technology companies are all investing in building first- and last-mile (FLM) transport solutions. Furthermore, driverless technology is expected to make these solutions even more efficient and safe. However, there are still a few challenges hindering wide-scale deployment of these solutions. In this context, Dubai launched its World Challenge for Self-Driving Transportation in 2018–19, with focus on FLM connection to test technology maturity and supporting technical development, public awareness and policy development.

First- and last-mile solutions

Transport authorities worldwide are encouraging FLM solutions, as they enable people to use public transportation. Companies are investing in developing and testing prototypes of autonomous FLM solutions to increase efficiency and safety on roads. Navya (France), EasyMile (France), 2getthere (the Netherlands), Westfield (the UK) and Gaussin (France) are the leading companies that offer the most advanced solutions in autonomous FLM transportation. Details of their offerings are captured in Figure 4.

As can be seen in the figure, the solutions still vary in technological maturity and technical specifications. All five offered solutions are SAE Level 4 in autonomous driving and currently being tested on designated routes in restricted zones, such as shuttle services for universities, airport connections and campuses of private companies. The growth of autonomous FLM transportation has also spurred activity among technology start-ups to develop vehicle-to-everything (V2X) connectivity, analytics, safety and smart solutions. Leading start-up players include Derq, Sensible 4 and iAuto.

Challenges in deployment of autonomous first- and last-mile transportation

Despite the technological advancement of autonomous shuttles, there are still a few challenges that hinder wide-scale deployment. The key challenges that transport authorities need to be mindful of to ensure successful adoption of driverless shuttles are:

- Building perception of safety and trust.

- Educating people on using the service and operating in public spaces.

- Building low-cost and environmentally sustainable charging options.

- Handling the fear of driver job losses.

- Ensuring financial sustainability of the business.

- Influencing pedestrians, cyclists and other vehicle users’ behavior.

To address these challenges, public transport authorities need to proactively develop policy frameworks and strategies to shape the autonomous FLM transportation segment. Since autonomous FLM transportation technology is in nascent stages of development and adoption, authorities need to invest in building adequate ecosystems via levers such as adaptive regulations, funding, capabilities building, organizing competitions to encourage innovation, testing autonomous technologies/infrastructure, and creating public awareness.

Dubai World Challenge for Self-Driving Transportation

(Focus on FLM connections)

Dubai has been at the forefront of the autonomous transportation wave and aspires to have 25 percent of all its transportation trips as smart and driverless by 2030. To realize this vision, Dubai’s Roads and Transport Authority (RTA) launched the “Dubai Autonomous Transportation Strategy”. As part of the strategy, Dubai organized its World Challenge for Self-Driving Transportation in 2018–19 as a global RFP to encourage the world’s most innovative international companies, academic institutions and centers of R&D to test the latest advances in this technology by providing transportation solutions and scenarios that were realistic and tailored for Dubai. The challenge was launched with a focus on first-/last-mile transportation:

- Objectives: The challenge aimed at providing a platform to leading players to showcase their automated driving technologies for first-/last-mile connections, demonstrate use cases, and support technical development, public awareness and policy development. In addition, it helped showcase Dubai’s brand as an international leader in transport and smart city technology.

- Use cases: Three use cases were identified: (a) self-driving vehicles (SDVs) connecting origin/destination to public transport, (b) SDVs connecting off-site parking lots to venue entrances, and (c) SDVs transporting people around certain locations/developments.

- Participants: Out of 65 initial participants, five leaders (SDV manufacturers Gaussin, Westfield, Navya, 2getthere and EasyMile), three start-ups (Derq, Sensible 4 and iAuto) and eight academic bodies (local universities – Abu Dhabi University, Al Ain University, UAEU, University of Dubai; and international universities – Carnegie Melon University, University of Technology Sydney, Universidad Carlos III de Madrid, University of Berlin) were selected for the challenge.

- Testing: A testing site was chosen based on access, testsite architecture, infrastructure and flexibility/availability. Twenty-one test cases were set up at the circular test track to be performed by the vehicle under test. (Please refer to Figure 5 for more details on the track and test cases). Participants drove the circular tour multiple times, with its complexity increasing with every round. Examples of complexity levers were speed levels, Dubai-specific environment constraints, staged mixed traffic, and obstacles (e.g., parking cars, construction zones). The vehicle under test was equipped with measuring equipment to record key evaluation parameters such as position, speed, acceleration, and time.

- Evaluation: Each participant group had to deliver a presentation to demonstrate its technical capabilities. However, since each participant group had different levels of technological maturity, different testing focus and procedures were applied:

- Leaders tested their vehicles on the challenge test track.

- Start-ups gave live demonstrations of technology functionality.

- Academia focused on demonstrating work-model functionality – either live or in simulation.

Participants were evaluated on seven competence fields – business model, endurance and reliability, energy efficiency and environmental suitability, consumer experience, safety & cyber security, staged mix-traffic, and simulation and new concepts. As an output of the evaluation, Navya and Gaussin were the winners in the Leaders category, with Navya’s vehicle demonstrating high durability and reliability and displaying exemplary customer experience, and Gaussin’s vehicle ranking highest in energy and sustainability.

A key learning from the Dubai SDT challenge was that one of the biggest hurdles in autonomous FLM transportation was passenger safety. The Roads and Transport Authority in Dubai recognized this concern and made it a topmost priority. They tested the autonomous technologies in different use-case scenarios and constraints, simulating different possibilities for obstacles faced on roads. The challenge received global acknowledgement for its robust testing approach and was a big success, attracting more than 700 technology leaders and innovators, as well as around 3,000 visitors for the accompanying exhibition.

City of the semester

Focus on Dubai

Autonomous technology is redefining the future of urban mobility and public transport. A revolution is on the horizon, from cars to buses to marine transport. OEMs, technology companies and transport authorities are joining the race to deploy selfdriving transport, establish their leadership positions in this fast-paced environment, and reap the multiple benefits it can deliver. In this context, the Road and Transportation Authority (RTA) of Dubai has defined the Dubai Self-Driving Transport (SDT) Strategy, which aims to achieve 25 percent of all transportation trips in Dubai as smart and driverless by 2030.

Dubai Self-Driving Transport Strategy overview

As a part of Dubai’s smart city strategy, His Highness Sheikh Mohammad bin Rashid Al Maktoum launched the Dubai Smart Self-Driving Vision, stating, “By 2030, 25 percent of all trips in Dubai will be driverless.”

To achieve this ambitious vision, RTA has developed the Dubai Self-Driving Transport (SDT) Strategy, which provides a vision, roadmap, and policy framework comprising a strategy for testing, development, and deployment of SDT.

The uniqueness of the Dubai SDT Strategy is its focus on multimodal transportation. Indeed, while most other cities and countries are focusing on selected transportation modes, Dubai is targeting SDT across all modes of public transport, including metro, tram, bus, taxi, marine transport, cable cars and shuttle.

As depicted in Figure 6, the self-driving Metro is currently the only transport mode contributing towards SDT, accounting for approximately 9.5 percent of all individual trips in Dubai. However, by 2030, the 25 percent target will be achieved via application of SDT technologies to other transport modes.

Dubai Self-Driving Strategy roadmap

RTA has developed a comprehensive Dubai SDT roadmap that considers not only SDT technology readiness, but also the infrastructure and legal requirements at the base of SDT deployment.

In addition, the Dubai SDT roadmap has been tested with the support of SDT experts in the field of SDT technology, as well as infrastructure and insights drawn from conducting a series of workshops with the major OEMs and start-ups leading the SDT ecosystem.

For each transportation mode, the following implementation plan will be executed in Dubai, to achieve 25 percent SDT by 2030:

- Bus transport mode

- In 2023, RTA will start conducting the first commercial trials of a limited number of L3 smart buses. L3 smart buses will require the presence of a human driver. Operation in automated mode will be possible only in simple operational design domains (ODDs), with limited interaction with mixed traffic.

- In 2028, RTA will launch the first L4 buses. L4 buses will be driverless and capable of operating in automated mode in simple and complex ODDs (e.g., complex urban roads), with full interaction with mixed traffic.

- Taxi transport mode

- In 2023, RTA will introduce L4 community taxis. L4 community taxis will be driverless and capable of operating in automated mode only in limited ODDs, within some communities of the city of Dubai (e.g., Jumeirah Lake Towers, Downtown).

- In 2028, RTA will launch L4 “everywhere” taxis. L4 everywhere taxis will be driverless and capable of operating in automated mode across all HD-mapped areas of Dubai in both simple and complex ODDs.

- Shuttle transport mode

- In 2020, RTA will conduct the first trials and start small rollouts of L4 shuttles. L4 shuttles will be driverless and capable of operating in automated mode only in very simple ODDs, with limited interaction with mixed traffic.

- In 2025, RTA will introduce L4 dynamic shuttles. At this stage, shuttles will still be driverless and able to operate in automated mode on both simple and complex urban roads, with full interaction with mixed traffic. In addition, these vehicles will operate on pre-programmed routes with dynamic features

- Marine transport mode

- In 2021, RTA will introduce lake vessels, autonomous electric abras that will operate on the artificial lakes of Dubai (e.g., Burji Khalifa, Global Village). These vessels will not require the presence of supervisors on board but be remotely supervised by operators from an operation control center (OCC).

- In 2024, Dubai will introduce canal and coast vessels, autonomous vessels which will operate along the coast and canals of the Dubai. These vessels will require human presence on board, but only in an engineering/ safety role. These vessels will still be remotely supervised by operators from an OCC.

- Beyond public transport

- Beyond public transport, other modes, such as personal SDT passenger vehicles, autonomous aerial taxis, SDT logistic bots, and SDT logistic drones, will be gradually introduced to contribute towards the achievement of the 25 percent by 2030.

The implementation plan does not include Metro and other rail public transportation modes since their systems are already automated.

Dubai Self-Driving Strategy enablers

To accomplish its vision, Dubai should focus on the following self-driving strategy enablers to guarantee execution of its ambitious implementation plan:

- Regulatory readiness: Dubai should lead in developing policies and legislation to allow full operation of selfdriving vehicles on its public streets. Legal and regulatory components such as liability and insurance, data privacy and cybersecurity, and SDT vehicle licensing and registration should be amended in order to accelerate SDT rollout.

- Infrastructure readiness: Better and smart public transport infrastructure elements such as service depots, vehicle stops, and road layouts will be required to allow implementation and operation of SDT vehicles. These are some elements that RTA needs to be mindful of when planning future SDT rollout.

- Technology/system readiness: SDT deployment also requires enhancement of certain technology/system elements such as control centers, fare collection systems, network connectivity, cyber security and HD maps. These will enable vehicle connectivity and ensure a safe SDT rollout.

- Customer acceptance: Creating customer acceptance is key for SDT deployment. The biggest hurdles to customers’ acceptance are their concerns about the cybersecurity of connected cars and the reliability of cars with autonomous functions. Dubai should conduct several surveys and focus groups to understand how to increase the overall acceptance of SDT.

Interview of the semester

Interview with Joby Aviation’s Executive Chairman by Antonio Semeraro – Manager at Arthur D. Little Middle-East

Joby Aviation is a venture-backed aerospace company that is developing and commercializing a piloted all-electric vertical take-off and landing (eVTOL) aircraft that can enable a fast, quiet, and affordable air-taxi service. Joby Aviation competes against other companies developing eVOTL aircrafts, mainly large traditional companies such as Bell, Boeing and Airbus, and start-ups such as Lilium and Volocopter. It distinguishes itself with its relatively mature aircraft technology and service offering. The company claims it is “100 times quieter than conventional aircraft during take-off and landing, and near-silent when flying overhead.” Last January, it raised another USD 590 mn in a Series C funding round led by Toyota Ventures, which increased its total funding to USD 721 mn. We had the pleasure of conducting an e-interview with Paul Sciarra, the executive chairman at Joby Aviation and co-founder of Pinterest.

Mr. Paul Sciarra is the executive chairman of Joby Aviation and co-founder of Pinterest

Q: Could you give us a brief background on Joby?

A: Joby Aviation is an aerospace company that is developing and commercializing a piloted all-electric vertical takeoff and landing (eVTOL) aircraft that can enable fast, quiet, and affordable air-taxi service. Ten years ago, we set out to improve daily transportation. Increased congestion, underfunded infrastructure, and rising emissions led us to design a new class of electric aircraft – one that can get you to where you are going up to five times faster than driving, at a cost that can approach car travel, and with zero emissions.>/p>

Q: How do you define Urban Air Mobility (UAM) at Joby? What is your vision?

A: “Urban air mobility” was coined by NASA and most recently changed to “advanced air mobility” – you can read more about it here: https://www.nasa.gov/aam.

Our vision is to bring fast, quiet and zero-emissions air mobility to communities worldwide that will change how we connect people with the places they live, work, and play in.

We’re happy that the industry has shifted from just urban air mobility to advanced air mobility. Everyone – whether in cities, suburbs or rural communities – wants to get where they are going more quickly. If the problem in cities is overcrowded roads, the problem in some rural areas is non-existent ones or inconvenient routing. We’ve designed a vehicle that we believe can solve both problems for both types of communities.

Q: What is the target position of Joby in the UAM ecosystem?

A: First, the aircraft.

We are bringing to market the most advanced and comfortable eVTOL aircraft, optimized for air-taxi operations.

Then, the service.

We will not only build the vehicles, but also operate them in communities worldwide.

Q: Why do you see great potential for UAM, and what future use cases do you see?

A: We aim to deliver safe, quiet and increasingly affordable air transportation to everyone, for any trips two to 150 miles. Those could be one-off trips or your daily commute. We want to make it faster and safer to get you where you’re going.

Q: How do you envision the future business model of UAM?

A: We’re not only designing, building and certifying the aircraft; we’re also operating the service – delivering air transportation directly to passengers.

In many ways, it’s actually a not-uncommon model in the history of aviation. In the early days of air travel, Boeing owned United. They not only designed and built airplanes, but also operated them as a commercial carrier. We’re heading “back to the future” with this approach.

Q: For UAM deployment in a city, who are the main stakeholders involved in the deployment and what are their roles? How can different stakeholders work together to support aerial vehicle deployment?

A: We’re actively working with several city governments, local communities and private property owners to build support and infrastructure for the service. It’s still early, but the reception, so far, has been encouraging.

Q: Which vehicle will Joby introduce initially?

A: Joby Aviation’s aircraft is designed for four passengers plus a pilot. We made the decision very early to make provisions for a trained pilot in-seat – both to ensure our passengers feel safe and comfortable, and to ease integration with existing air-traffic control (which is still based on humans talking to other humans over radio).

Q: Where do you see UAM being implemented initially? Has Joby identified potential markets for initial operations?

A: We expect to see AAM initially implemented on routes that have a lot of people moving in both directions. Airports to city centers are a good example. Nearby city-pairs are another.

We are not quite ready to discuss details of Joby’s initial launch markets. We can say we’re actively evaluating several options.

Q: What is the main issue regarding public acceptance, and what steps can be taken to overcome this?

A: It’s critically important that we earn the public’s trust when it comes to the safety of our vehicle. We started with the design, which is doubly and, in some cases, triply redundant across all critical subsystems to avoid any single points of failure. We’ve begun the type certification process with the US FAA to ensure – through rigorous testing at the component, the subsystem and the vehicle level – that the aircraft meets or exceeds the highest safety and reliability standards.

Q: What is the major challenge going forward?

A: Right now, we are squarely focused on certifying the aircraft and getting ready for initial production of the aircraft. We expect to break ground on a new factory shortly.

We’re in the hard business of aircraft development and certification because the right certified vehicle is the key to unlocking this market.

Q: How are different regulators responding to UAM deployment?

A: Joby has been working with the FAA for several years and began a formal type certification program in 2018. The type certification process assures the safety of the vehicle and typically takes three to five years.

We’ve been extremely impressed with the diligence and creativity of our counterparts at the FAA. Fundamentally, they care about the same thing we care about: the safety of the aircraft and its passengers.

Joby is also in discussion with a number of international regulators regarding the parallel certification paths and ex-US, commercial operation of our aircraft.

Q: What is/will likely be the key impact of COVID-19 on your business and the autonomous industry in general?

A: It’s hard to predict the impact of COVID-19 on our business as we look ahead to commercial launch, a few years away.

Right now, we’re focused on ensuring our employees are safe, and contributing where we can in the communities where we operate.

DOWNLOAD THE FULL REPORT